The New Mississippi: John Law vs Elon Musk

Anatomy of a Systemic Sovereign Amplified Bubble

Three hundred years ago, a Scottish gambler named John Law built a financial machine that bankrupted France and gave birth to the word “millionaire.” Over the last 25 years, Elon Musk has built a strikingly similar machine. Tomorrow night, twenty-one banks put their stamp of approval on the modern version - the SpaceX IPO.

Before we embark on this journey of exploring the Mississippi Bubble and how it relates to our modern situation, I would just like people to know that this will be the first of 50 essays I write on the topic of Capital Misallocation. We live in historic times and my original reasoning for choosing this name for my Substack and Twitter handles was to explore this topic. With the help of my new interns, aka AI agents, I have narrowed down the list of the Top 50 Episodes of Capital Misallocation TM that have occurred over the last 400 years. I will explore the philosophical and mathematical misperceptions and rehash these historical moments with an angle of trying to relate them to what we are living through today. I am happy to get back to writing as two decades of being a trader and PM on Wall Street distracted me from writing as much as I would have liked to over the years.

Benny & The Squirrel & SpaceX

If you are interested in detailed analysis of the SpaceX IPO, The Blind Squirrel and I have covered the deal at length over the last two months on our podcast Benny & The Squirrel as well as on this site where we published two reports - “Spaced Out” in early April & “SpaceX: What Wall Street isn’t Telling You”.

Tomorrow evening, after the close, a syndicate of underwriters full of gentlemen, whom modestly resemble a younger version of The Squirrel, will gather physically, or more likely over a zoom call with at least one person who should be on mute who forgot to hit the button, and set the final price on 556 million shares of Space Exploration Technologies Corporation. The deal price is set to be $175 - implying a $75 billion equity raise and an implied valuation of $1.75 trilllion.

On that same evening of the deal consummation, The Squirrel and I will be hosting an episode of our podcast - Benny & The Squirrel - with former Bank of America ECM deal captain Craig Coben. Craig will be just another of the many guests on the podcast who joined us from a third continent for the show proving that Benny & The Squirrel have definitively solved “The 3 Body Problem” of podcasting. In all seriousnous, it will be a blast to record on the evening of the largest IPO in history with two former major bank equity capital markets deal captains. Then Friday morning, many hours after all of us finished the show, the ticker SPCX will go live on the Nasdaq completing the largest and most controversial IPO in history.

I want to be clear about the magnitude of this deal, because “largest IPO in history” has lost its punch over the years I have been in the game. Saudi Aramco - a company that pumps the literal lifeblood of industrial civilization out of the ground at a cost of about three dollars a barrel - completed a deal that raised $29 billion in 2019. Now lets compare that to SpaceX, which is raising 2.5 Aramcos in this capital raise to fund, among other things than the $25b bridge loan repayment, data centers in outer space - so sexy that it almost makes me want to pay 100x revenue for that paper!

The Squirrel & I have chatted and are confident that the financial press will spend Friday debating the first-day pop. I would like to spend a little of your time today pondering a different question. Namely - what kind of object is this that is coming into our orbit up close and personal?

A Trip Back to the Early 18th Century

To answer the question posited above, join me on a trip to the summer of 1719, when the most valuable real estate in Europe was a muddy alley in Paris called the Rue Quincampoix.

That particular location wasn’t valuable for what was physically on it but for what was happening on it. From dawn until well past dark the street was packed shoulder-to-shoulder with dukes, merchants, soldiers and servants, all of them screaming prices at each other for shares in one company. Legend has it that an enterprising hunchback supposedly made a small fortune renting his back out as a writing desk so traders could sign contracts faster - a story that remains, 300 years on, one of the most pure expressions of “picks-and-shovels” investing in recorded history. It was so insane that there are stories of a coachman getting rich enough to hire two coachmen, one of them kept to himself. Men who were broke and destitute in April were buying châteaux by October. France didn’t have a word for what was happening to its citizenry, so it’s citizens created one that is so ubiquitous today that is hard to imagine life without the term.

Millionaire

The company was the Mississippi Company. The man who built it was a Scottish gambler, a convicted murderer, and a self-taught monetary genius named John Law. For about eighteen months Law was effectively the richest and most powerful private citizen on Earth. He ran France’s central bank and France’s largest corporation at the same time, which means that he controlled both the money and the thing the money was used to buy - namely a claim on the “Mississippi Company”. Law had effectively talked a bankrupt empire into handing him the keys to the treasury.

By the end of 1720 it all crumbled and his short-lived empire became a pile of rubble. Law fled France in the dead of night apparently with one decent diamond but effectively broke, yet one step ahead of a mob that wanted him dead. The trauma was so deep France refused to use the word banque near its financial institutions for the better part of two centuries. John Law died in Venice nine years later in 1729, broke yet still playing cards - a true gambler to the end.

I bring this up because we are witnessing the modern day John Law run the experiment once again at a scale that would have made John Law dizzy. And, thanks to Elon, in this particular spot in space time our society has even coined an upgraded term for extreme wealth that can only be sufficiently described using a power law framework.

Trillionaire

The Thesis: Not a Bubble. A System

Let’s be clear on something right from the start so I don’t lose readers who come in with a bias on the modern John Law.

I am NOT saying Elon Musk is a fraud. He’s a once in a generation entrepeneur whom, I believe, will hold a permanent place in the history books.

John Law was NOT a fraud either. In fact, Law was in fact a legitimately brilliant monetary theorist whose ideas got vindicated centuries later.

I’m NOT saying AI is fake.

I’m NOT saying SpaceX doesn’t launch real rockets. I’m NOT calling any of this a con. Just needed to get that out of the way to shake off all the Elon loving trolls.

What I’m saying is structural. The current AI and space boom going on at the moment, and specifically the Musk empire sitting right in the middle of it, isn’t just another tech bubble like the dot-com boom. That bubble was more akin to a thousand small fires of retail enthusiasm all residing within the same vacinity.

In comparison, today’s version resembles something older and meaner - a System. A system that is a self-reinforcing machine where private corporate ambition fuses with sovereign state power and circular financing to manufacture the appearance of growth. If you are a mechanical engineer or a tourist in studying systems then you know that systems have signatures. They have to keep fueling the machine and expanding to survive. Confusing recycled capital for real revenue is a hallmark trait of this particular system that Law & Musk mastered. Systems end differently than bubbles do as bubbles eventually burst and sting the participants with some momentary pain. When systems ultimately unwind they take pieces of the monetary system of that particular point in space time down with them. For example, France didn’t just lose money in 1720, it lost the ability to have banks or even muster the ability to say the word banque. I mean not to unlike how housing or shale or railroads became pariahs in the aftermath of their respective bubbles to be fair.

We know how this movie ends. We’ve seen it. We just don’t know what minute we’re on, however, just as when we watch great films, we hope it never ends. No matter what you think about Elon or Trump, it is hard to deny that this has diminished the need for fiction as we seem to be living in the most entertaining period of time in history.

So let me walk you through the parallel step by step.

Once you see it, like The Squirrel in this video, you won’t be able to unsee It.

ACT ONE

The Visionary Outsider

The son of a goldsmith, John Law was born in Edinburgh in 1671. For those who weren’t paying attention during 17th century French history class, a son of a goldsmith was effectively the same as being the son of Jamie Dimon, or a lesser version of a banker, in that goldsmiths held deposits and issued paper receipts, the prededecessor of fiat money, against those deposits. Although I couldn’t find the exact moment credited to his epiphany, I did learn that there was a moment in Law’s childhood when he aborbed the single most dangerous idea in finance - that paper receipts circulate whether or not anyone checks the vault.

By his twenties, Law had compressed several lifetimes of trouble all into one : he killed a man named Beau Wilson in a duel over a woman, he was sentenced to hang, he escaped prison prior to judgement, and then he escaped from the land of fine whiskey and bolted to the continent that we now refer to as Europe.

Law wasn’t really a gambler though. He was a theorist who happened to gamble. In his head he was building something: the heretical idea that nations should ditch gold-backed money and run their economies on paper currency managed by a central bank. Credit, not metal, was the fuel.

For its time this was nuts. Karl Marx later described Law as having “the pleasant character mixture of swindler and prophet.” Alfred Marshall called him “a reckless, and unbalanced, but most fascinating genius.” Both were right. That’s the thing about this archetype. The swindler and the prophet aren’t two different people. They’re the same person. You only find out which one you were dealing with at the end.

Law shopped his system to anyone who’d listen. Scotland passed. England passed. The Duke of Savoy passed. Louis XIV passed. The most important monetary thinker in Europe couldn’t get a single sovereign to pick up the phone.

Hold that image, and look at the other guy.

Elon Musk got to America by way of South Africa and Canada, carrying his own heresies: cars should be electric, rockets should be reusable, machines could think. He had his own thing with the authorities — tangled with the SEC, settled the funding-secured tweet, paid twenty million dollars and gave up his Tesla chairmanship. Depending on who you asked he was a once-in-a-generation genius or a dangerous huckster. And he, too, was right enough times that the sheer force of his conviction became gravity. Capital bent toward it.

Here’s what matters. Both men sold themselves as the cure for a sick country. Law was going to fix France’s post-war debt with financial alchemy. Musk was going to fix America’s bureaucratic flab and tech complacency with radical efficiency and frontier swagger. And both of them understood the single most important move in the playbook:

You can’t build a System alone. You need a sovereign patron willing to hand you power no private citizen should ever have.

Law found his sovereign in the form of Philippe II, Duke of Orléans and Regent of France. Philippe II was a man desperate enough to dodge national bankruptcy that he was willing to try anything, including giving the keys to the castle to a brilliant persuasive “genius” gambler. Not too unsimilar to today.

Elon Musk followed Law’s lead and found his sovereign in the form of Donald Trump.

ACT TWO

When the Gamekeeper Becomes the Poacher

Here’s where the structure stops being a vibe and starts being mechanical.

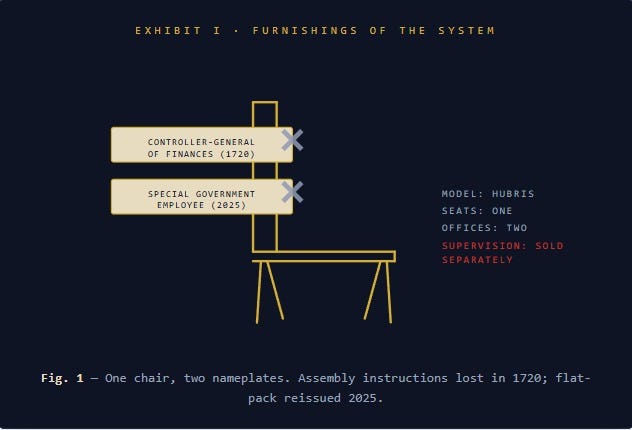

In 1716 Law launched the Banque Générale, a private bank licensed to issue paper notes. In 1717 he founded the Mississippi Company, with a monopoly on French Louisiana. Then he started consolidating, and he did not stop. By 1719 he’d swallowed every other French colonial trading company. He took over tax collection. He took over the royal mint. He absorbed the national debt itself, swapping it into shares of his own company. In January 1720 the Regent appointed him Controller-General of Finances, which at the time was the most powerful financial office in France and is akin to being a central banker or treasury secretary in today’s world.

By early 1720 John Law personally controlled the money supply (his bank, by then nationalized as the Banque Royale) and the primary asset the money was being used to buy (his own company’s stock). He was the central banker and the CEO at the same time. He set the price of money and he sold the thing you bought with it.

The conflict of interest wasn’t a bug in the system. It was the System.

Elon Musk’s version of this dynamic is messier and more modern, but the bones are the same. By early 2025 he’s sitting on a truly impressive collection of assets - Tesla, SpaceX, xAI, X, Neuralink, the Boring Company. Then Trump installs him as head of the Department of Government Efficiency, or commonly referred to as DOGE in a play on the crypto token. The kicker is the access Musk was granted on this appointment such as access to unclassified federal records, government IT systems, and a perch overlooking the exact regulations and contracts flowing back to his own companies.

The Economic Policy Institute did the math in 2025 and reported a doubling in federal contracts to Musk’s various companies. Elon has now publicly admitted advising the President on tariff policy that directly benefited Tesla. In addition, he stood in front of the White House to talk up the stock price of Tesla. And, he was actually the guy who oversaw agencies that were cutting multi-billion-dollar checks to the company going public tomorrow - SpaceX.

Gamekeeper and poacher. Regulator and regulated. One guy, both chairs.

Three hundred years apart. Same impossible seat.

Controller-General of Finances, c. 2025. Bring your child to apex-hubris day

ACT THREE: PART ONE

The Engine That Eats its Own Tail

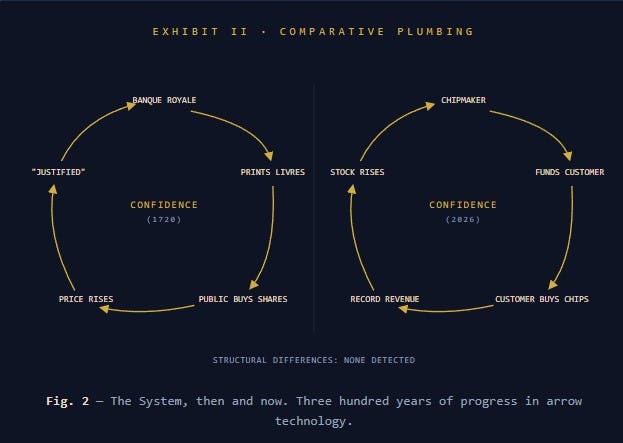

If the merger of state and private power is the Body of the System, circular financing is the bloodstream. This is the part everyone underrates because it looks like growth right up until it looks like a crater.

Here’s how Law’s loop worked. The Banque Royale handed out loans at a friendly 2% to ordinary speculators. The speculators used the borrowed money to buy Mississippi Company stock. The company itself also bought its own shares, financed by loans from the same bank. Price went up. Higher price justified more lending, which financed more buying, which pushed the price higher. In February 1720 the bank just printed 300 million livres for the express purpose of buying Mississippi shares.

The money was eating its own tail just like an ouroboros.

The “revenue” was, in big part, the System recycling its own capital and calling the echo a heartbeat.

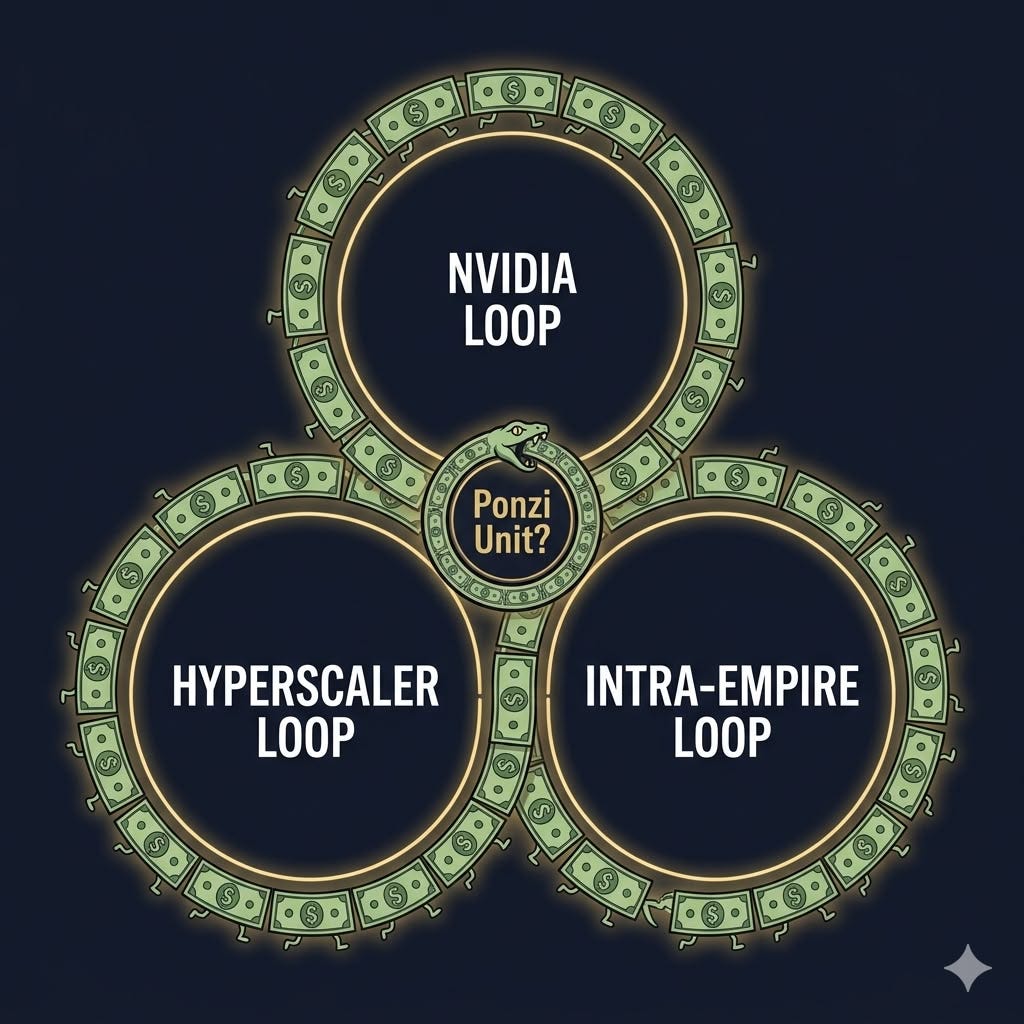

Now lets look at 2026. Three loops, because if you only know one of them you’ll let yourself off the hook too easily.

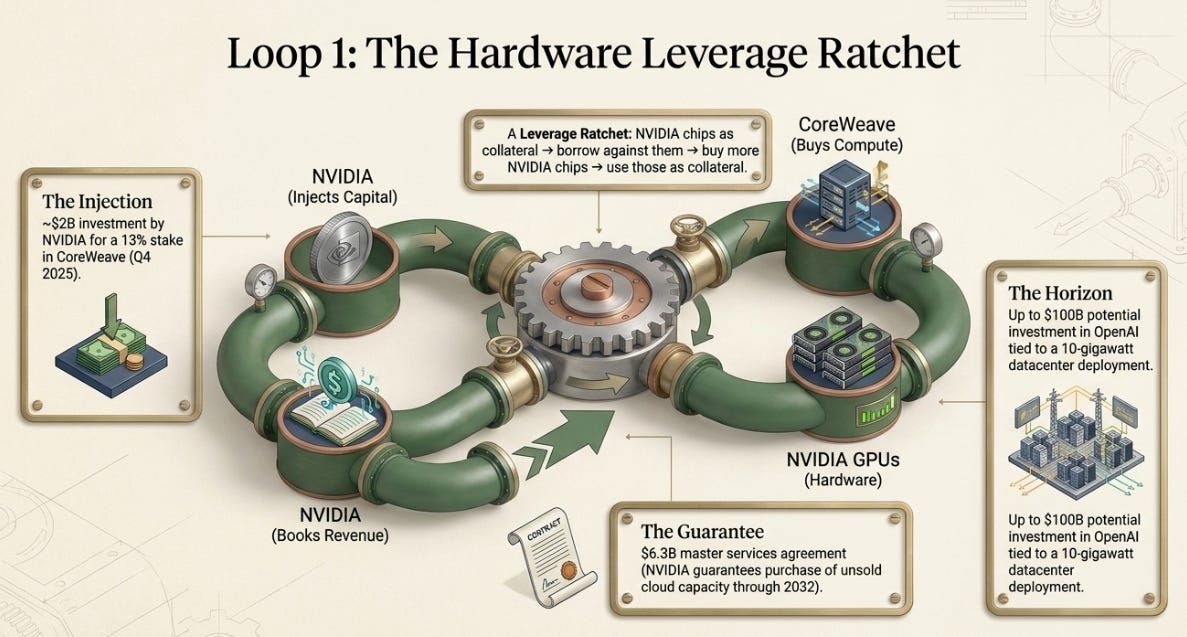

Loop One: Nvidia

Nvidia sells GPUs to AI companies and then also turns around invests in those same AI companies. It is well obvserved by many commentators and market participants on NVDA’s role in funding Coreweave - a large buyer of its GPUs over the last couple years. NVDA was an early investor, it anchored its IPO to get it across the finish line, and funded its loan last year when the market was unwilling driving its CDS spreads down from 900bps to the current 500bps level. In addition, a few other examples include a reported $100 billion commitment to OpenAI and a multi-billion-dollar stake in xAI. The recipient companies of the money use the cash to buy more Nvidia chips and then Nvidia books the chip purchases as revenue. The revenue lifts the stock which then acts as collateral to funds more investments in the customers and enrich the owners and employees.

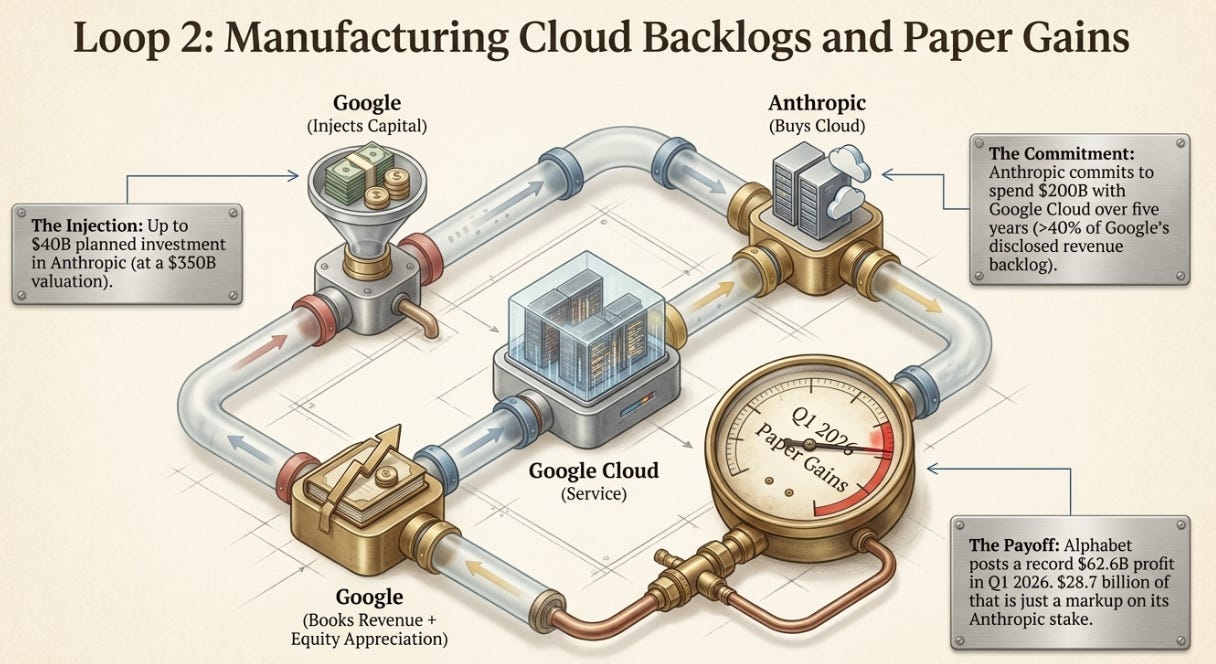

Loop Two: The Hyperscalers

Microsoft and Oracle buy enormous quantities of Nvidia chips, rent the compute to AI startups, and invest in those same startups whose “revenue” is, in meaningful part, the cloud spending those investors handed them in the first place. The cloud giants then report that spending as roaring customer demand. Google and Amazon do this as well with Anthropic committing to enormous cloud commitments and buying Google’s TPUs. The funny thing about the Google/Anthropic arrangement is that Google’s equity stake actually represented almost half of its record Q1’26 earnings due to simple “Gain on Sale” accounting.

Loop Three: The Intra-Empire Loop

This is the one that should make the hair on your neck stand up, because it’s the purest Law parallel. As we noted on Benny & The Squirrel, the SpaceX S-1 noted that Tesla put $2 billion into xAI. xAI bought $430 million of Tesla Megapacks. SpaceX then absorbed xAI entirely. The combined entity is now marching toward an IPO whose valuation will be used to validate every internal price set along the way. Money moving from Musk’s left pocket to his right pocket, and the market applauding the bulge.

This isn’t a conspiracy theory. Every one of those transactions is in public reporting. It isn’t secret. It’s structural. Soros named it decades ago: reflexivity. The feedback loop where prices don’t just reflect reality, they bend it. A rising valuation validates the investment that pushes the valuation higher, which draws the capital that lifts it again. Going up, reflexivity looks like vision. Problem is, the same machinery runs in reverse — and structures don’t care whether you believe in them.

So how fragile is it?

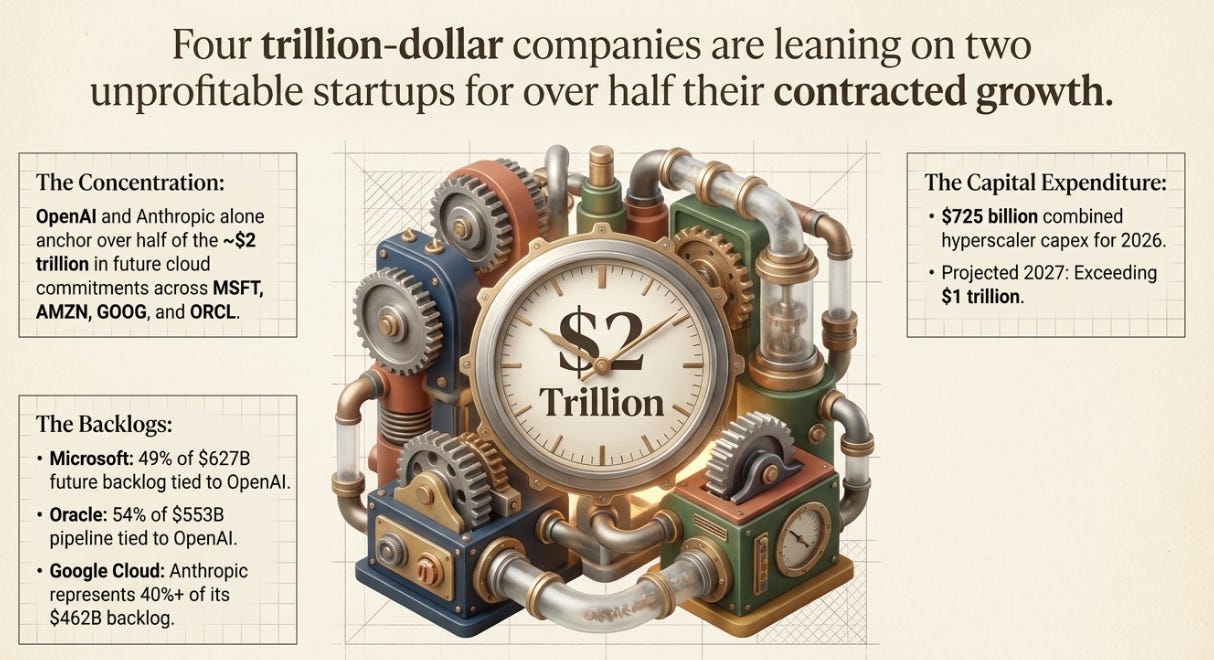

Look at the spread between what’s going out and what’s coming in currently. Consensus estimates have the AI sector deploying around $750 billion in 2026 and $1.1 trillion in 2027 in capex in against roughly $60 billion in revenue, which is roughly a 12:1 burn and requires the hamster wheel to keep spinning faster to try to catch one of Elon’s rockets and hit escape velocity. You can quibble with the exact figures but every hard number points in the same direction. Hyperscaler capex has exhausted its aggregate operating cash flow resulting in these names hitting the debt markets. And the bond market noticed resulting in these firms seeing their credit spreads materially widen. In fact, ORCL is essentially junk debt now in price if not in rating….yet. Then we saw last week Google do only its 3rd equity offering in history for a total of $80 billion only to be followed by META announcing a large $20 billion raise on Friday. For the first time in almost 35 years, the free cash flow at the largest tech companies on Earth is going negative. That’s the quiet sound of lenders pricing in the chance some of this doesn’t pay off - my advice is to keep a close eye on the credit market as we proceed on this circular funding credit fueled capex bonanza.

Minsky had a label for an enterprise that needs fresh capital every quarter just to stay current on the bets it already made. He called it a Ponzi unit. He didn’t mean fraud; instead, he meant a borrower whose own cash flow can’t cover its obligations and survives only by raising more. His darker point was that whole system drifts from hedge to speculative to Ponzi over the course of a long boom, and the drift is nearly invisible from the inside, because right up until the end everything still looks like it’s working.

Stability breeds instability. The calmer it looks, the more risk is piling up under the floorboards.

The spending is real. The data centers are made of actual concrete and silicon. But the revenue that’s supposed to justify it remains, to borrow a phrase, perpetually next year as we discussed in length in the last episode of Benny & The Squirrel.

ACT THREE: PART TWO

The Silver That Wasn’t There

Every System needs a story about the asset under it and for Law that story was silver. The Mississippi Company was supposedly sitting on the untapped mineral wealth of French Louisiana with endless silver waiting to be dug out and shipped home. The promotional engravings showed a paradise of riches. Investors weren’t buying a company. They were buying a promise about a continent most of them would never see.

There was, of course, no silver. Not in any quantity that mattered. The whole valuation rested on the future extraction of an asset nobody had bothered to verify existed.

Now here’s where I have to be careful, because this is exactly the spot where lazy analogies go to die and as mentioned earlier I don’t want to step into the territory of calling Musk a fraud. He has pushed the envelope and even redrawn the boundaries but has yet to be condemned a fraudster on the level of John Law.

AI is Not Louisiana Silver

Most important caveat in the whole essay. Bolded so nobody can accuse me of skipping it as I am confident that LLMs work, image generators work, and coding assistants are genuinely transforming software development right now. The technology is real and it creates real value. Anyone telling you it’s all smoke is selling you something too.

But the question was never “is there value here?”

The question is “is the value proportionate to the capital being thrown at it and is there a true economic model here?”

And there the echoes of 1720 get loud. xAI, now folded into SpaceX at a quarter-trillion-dollar valuation, generated something like $250 million in revenue over its last six reported months all while losing $2.5 billion. A company valued at $250 billion, doing a quarter-billion in revenue, torching ten times that in losses. OpenAI, brushing up against $300 billion, is burning capital at a clip that would have impressed the Rue Quincampoix. And study after study keeps finding that the overwhelming majority of enterprise AI deployments produce no measurable impact on the bottom line. In the last two weeks KPMG and Bain have come out with studies showing this and everyone has heard about the Uber COO talking about how the company blew its token budget in 3-4 months. The potential for a pause in spending from the enterprise is a real risk.

The silver is real this time. I’ll grant you that. But it just may not be sitting where the prospectus says it is and the mine may cost more to run than the ore is worth.

ACT THREE: PART THREE

The Fracture

Here’s the part I couldn’t have written a year ago. A year ago this was a prediction. Now it’s a description.

The Mississippi System died in stages, and the stages matter. By spring 1720 the machine had become a perpetual-motion fantasy, it needed an endless drip of new money just to hold the share price still. On May 21, 1720 the government issued a decree cutting the value of banknotes in half and announcing staged reductions in the stock price. It was supposed to be a controlled landing. It was not controlled. The streets that had been full of speculators filled instead with people trying to get their money out. Bank runs. Food prices up sixty percent. An outbreak of plague layered on top, because why not. By December Law was finished — stripped of his office and fleeing the country he had briefly owned, with nothing to his name.

Now watch the modern sequence. It rhymes with eerie precision.

In May 2025, Musk hit the legal ceiling on his government role as special government employees are capped at 130 days a year and stepped back from DOGE. Within days the sovereign-private alliance that anchored the entire System detonated in public. Musk looked at Trump’s signature “One Big Beautiful Bill,” the centerpiece of the administration’s agenda, and called it a “disgusting abomination.” Trump said he was “very disappointed.” Musk threatened to start his own political party. The bromance that reshaped Washington imploded into a social-media knife fight in real time.

DOGE was supposed to run until July 4, 2026, the country’s 250th birthday but instead quietly died eight months early. By November 2025 the OPM director was telling reporters it “simply doesn’t exist” as a centralized entity. The pitch was $2 trillion in cuts but the reported results came in at a disappointing $215 billion - an order of magnitude miss.

The modern Controller-General had been dismissed. Not by royal decree this time. By political gravity. Same outcome, different mechanism.

But here is where Musk diverges from Law, and where the story gets genuinely dangerous. Law had nothing left when his government job blew up. Musk responded by consolidating his private empire and aiming it at the public markets.

In February 2026, SpaceX absorbed xAI, which had already absorbed X. It was structured as a triangular merger, a clever bit of engineering designed to wall SpaceX off from xAI’s mounting legal problems.

And now comes the peak. SpaceX is preparing to go public tomorrow in what looks like it will be the largest IPO in human history.

Let me put that valuation in human terms because The Squirrel and I already have put out the numbers in detail on our podcast and in two reports. They are asking the public market to value a combined entity at a number larger than the entire annual economic output of every country on Earth except about ten.

In the Mississippi story, Law’s appointment as Controller-General in January 1720 was the apex. Maximum hubris. Four months before the decree that broke everything.

The SpaceX IPO is the appointment as Controller-General. It’s the System reaching for maximum extension, asking the public to ratify a valuation the private market manufactured for itself.

If the market says yes and it trades well tomorrow, then some of the risk transfers from the insiders to the public shareholders. The secondary share selling will be what will be really interesting to watch as we proceed.

If it says no, either tomorrow or over the course of the rest of the year, then the unwind starts

Where this analogy breaks (and why I’m telling you)

I don’t trust anyone who sells you a historical parallel without showing you where it cracks. Law controlled the literal money supply. Musk does not. The Banque Royale printed livres on command. The Fed is, on paper, independent. So the modern equivalent of money-printing isn’t one lever, it’s distributed across private-market valuations that bootstrap themselves through circular investment, venture capital that marks assets to model instead of to market, and stock prices that double as collateral for the next round of borrowing. Same effect with artificial liquidity holding up artificial prices, but you can’t kill it or save it with a single decree. Which, honestly, might make it harder to stop, not easier.

Tesla is a real, profitable, operating business.

The Mississippi Company had no meaningful revenue whereas Tesla sells almost a hundred billion dollars a year of actual cars and batteries and services. The Law parallel is sharpest on the private side of the Musk empire with the merry-go-round of intercompany transactions. Tesla is the public-market anchor Law never had, and it’s why this is a story about a part of the empire, not the whole man.

The strongest bull case is stronger than most bears will admit.

Here’s the best argument against everything I just wrote, stated as forcefully as its proponents do. Unlike the dot-coms, today’s hyperscalers are largely paying for this out of their own pockets until now so we need to see just how much leverage they are truly willing to take on to go after this global market share race.

Bulls like to point to the strong earnings companies are reporting and that are so responsibly funding the buildout are themselves, in part, are the end product of the recycled output of the loops discussed above. When Nvidia’s investment in a customer comes back as Nvidia’s revenue, that revenue becomes the earnings that “prudently” pay for the next wave of capex. The discipline is real on the surface and circular underneath. When the money is both the loan and the deposit, the ledger always balances. Right up until the day someone insists on being paid in something other than more ledger.

The ending is probably a repricing, not a zero. The Mississippi Company had no asset, so when confidence broke the price went to the floor. True binary. The AI complex almost certainly reprices instead a violent downward adjustment toward valuations that reflect actual cash generation rather than projected dominance. That can still annihilate anyone who bought the top. But it’s a haircut with a chainsaw, not a beheading.

The Doctor’s Cure

In 1752, three decades after the wreckage, David Hume sat down to think about what Law had done to France. He wrote a warning I have not been able to get out of my head:

…when the nation becomes heartily sick of their debts, and is cruelly oppressed by them, some daring projector may arise with visionary schemes for their discharge. And as public credit will begin, by that time, to be a little frail, the least touch will destroy it, as happened in France during the regency; and in this manner it will die of the doctor.

That’s the whole thing. It will die of the doctor.

Hume’s point wasn’t that the doctor was a quack. The danger was precisely that the doctor was brilliant — brilliant enough to be trusted with the diagnosis and the cure, and self-interested enough to profit from the treatment. Law diagnosed France correctly. His prescription contained ideas that became the foundation of modern finance. He just administered them at a lethal dose, with no safeguards, while getting rich off the patient.

Musk has diagnosed real problems too. The government really is bloated. AI really does require capital formation at a scale we’ve never attempted. Space infrastructure really will reshape the next century of geopolitics. None of that is fantasy.

The question for 2026 was never whether Elon Musk is a genius. The question is whether a System built on circular financing, opaque private valuations, and the fusion of state and corporate power can survive its first real contact with the cold scrutiny of public markets.

Law got his answer on May 21, 1720.

Musk may get his sometime after mid-June, when the SpaceX S-1 finally opens the books — and we all find out, together, how much silver is actually in the ground.

What I’m watching

I’m not in the business of telling you what to do with your money. But I’ll tell you exactly what’s on my screen, and you can draw your own map.

Tomorrow night’s print. Pricing above $135 on heavy oversubscription means demand is being rationed at the top of the range — peak-confidence behavior. The January 1720 appointment ceremony, with a bell.

The first-week retail flow. Whether the 30% retail allocation holds or flips. The Rue Quincampoix was loudest in its final winter.

Lockups and Form 4s. Law’s bankers converted to gold quietly. Insider filings are louder than they were in 1720. Read them.

Index fast-entry. The inclusion announcement, whenever it comes, is the forced-conversion edict. The passive bid it triggers is the last structural buyer of size. After the index buys, ask: who’s left?

Hyperscaler capex language. The first earnings call where one of them swaps “acceleration” for “optimization” is the first crack in the concrete.

Oracle’s financing calendar, CoreWeave, and the neocloud complex. The weakest, most leveraged links in the circular chain — and the credit market, which has been clearing its throat since September, is the adult in this room. Spreads doubling is how bond investors say “we’ve read about 1720” without alarming anyone.

Nvidia’s growth rate. The entire loop is load-bearing on one line item. The day it decelerates, the echo stops sounding like a heartbeat.

And then the big one — the modern May 21st. This is the one that haunts me, because Law’s fatal act wasn’t the inflation. It was the honest edict: the moment the architect acknowledged the gap between paper and reality and proposed an orderly schedule for closing it. Confidence is a thing you have until you ask whether you have it. So if you ever see the modern System’s principals propose a controlled deflation, a guided markdown, a “recalibration of expectations” with a timeline attached then I advise that you do not admire the responsibility but rather Run for the Exits.

One last thing about the vocabulary, because languages keep better books than banks do. French coined millionnaire in 1719, at the top, because the old words couldn’t describe what was happening to people’s net worth. English has trillionaire typeset and waiting for Friday’s close. But French gained a second word from the episode, and it’s the one that lasted: agioteur, speculator, manipulator of paper, which became one of the dirtiest words in the language for the next century, hurled at financiers right up through the Revolution, when several gentlemen who’d worn it met the national razor. The vocabulary of euphoria gets coined at the top. The vocabulary of blame gets coined on the way down, and it has a much longer shelf life.

Tomorrow night they set the price. John Law would have understood every line of the term sheet, admired the retail allocation, envied the index plumbing, and asked only one question and it was the same one he failed to answer in time:

What happens to a System when it stops growing?

He found out in eleven months.

We trade Friday.

First time here? I am a guy who has been on the buy side of the street for over 2 decades who has worked as an analyst at the largest asset manager in the world down to having my own shop trading special situations and macro to now having a volatility fund and being partners with a bunch of great people in various media and technology ventures. But now I am about to embark on the original mission of this substack blog - to chronicle and analyze historical episodes of Capital Misallocation TM - where the money’s going that shouldn’t be, what the implications are on a time weighted basis not just an ensemble average basis, and what happens when the music stops. We believe that markets and systems are non-egodic processes and that everything in society obeys power laws as they are just pieces of a larger complex adaptive system.

Subscribe and the next one shows up in your inbox. If you’d rather hear me and the Squirrel argue this out loud, the show’s on YouTube — @Benny_Squirrel.

If you are interested in real time trading insights and institutional level information flow then become a paid subscriber as I run a chat on here but really over Whatsapp and share all my thoughts, curiousities, trade ideas, and rants on there for paying subs.

Nothing here is investment advice, contact your financial advisor before making investment decisions and make sure you do your own work.

SLIDE DECKS BELOW PAYWALL:

The New Mississippi

The AI Circular Infinity Engine

Keep reading with a 7-day free trial

Subscribe to Capital Misallocation to keep reading this post and get 7 days of free access to the full post archives.