Republishing Article on Risk Off Warning - Own Convexity & SFRM5

Republishing a Note I Wrote on Wall Street Beats on May 31st

Republishing a note I wrote on Wall Street Beats on May 31st behind the paywall. If you would like to see more real time insightful analysis like this from me and my partners head over to Wall Street Beats. I promise you that you will get some good ideas and very sharp analysis from the bullpen of market veterans who have seen many cycles spanning over the previous decades.

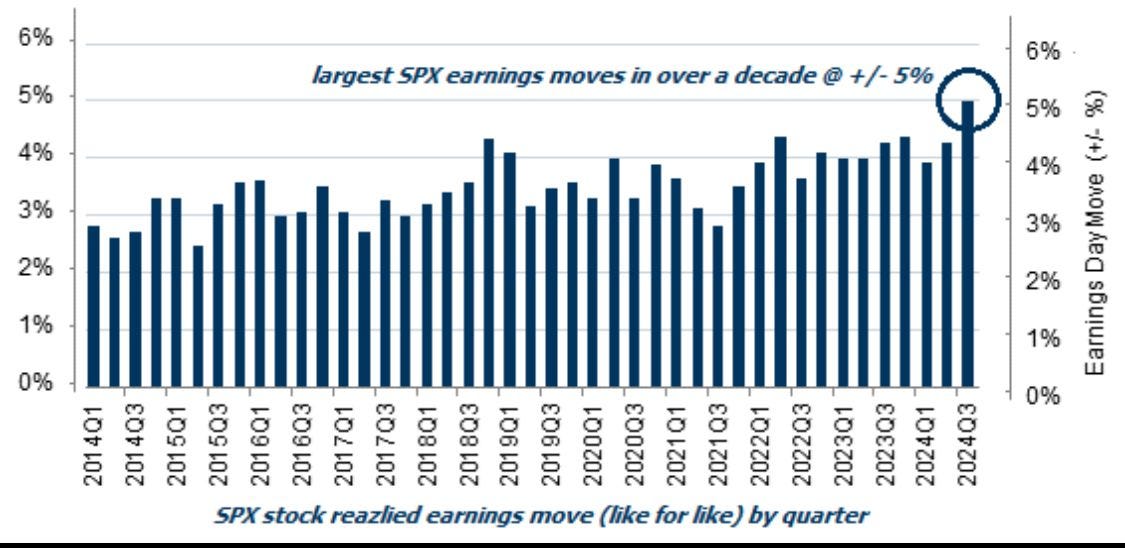

If you look around today we are in the most volatile earnings period since 2008.

Implied Correlation is Rising Along with Downside Implied Volatility - Liquidity is Dropping Fast

Keep reading with a 7-day free trial

Subscribe to Capital Misallocation to keep reading this post and get 7 days of free access to the full post archives.